Imagine this: You and a founder in San Francisco both launch a startup on the exact same day.

Over the next year, you both hit the exact same milestone: $1 million in Annual Recurring Revenue (ARR). The metrics are identical. The growth rate is identical.

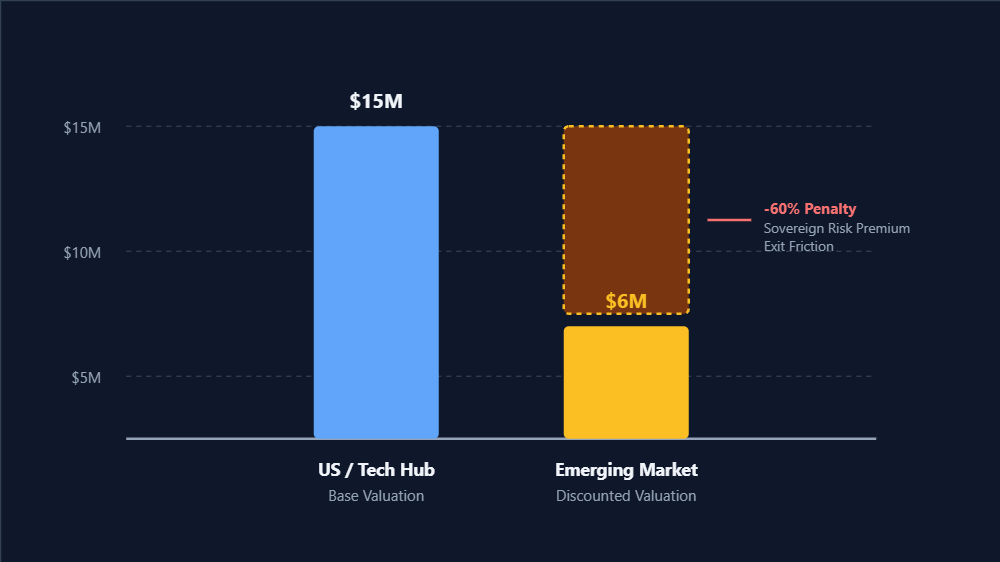

The San Francisco founder walks into a venture capital pitch and gets a term sheet for a $15 million valuation. You walk into a pitch with the same numbers, and the investor offers you a $6 million valuation.

If you are a builder sitting in India, Latin America, or Eastern Europe, this feels like a slap in the face. It feels like geographical bias. You are being punished simply because you aren't sitting in a coffee shop in the Bay Area, right?

Not exactly.

Investors don't care about fairness. They only care about math. And when you build a company outside of a major US tech hub, you are carrying a hidden weight that US founders don't have.

The Math Behind the "Penalty"

To understand why your valuation got slashed, you have to understand how a VC figures out what your company is worth today.

They use a formula called "Discounted Cash Flow" (DCF). In plain English, they guess what your company will sell for in the future, and then they "discount" that number backward to today based on how risky you are.

Think of it as a simple fraction:

Valuation = (Expected Future Exit) / (The Risk Factor)

The bottom part of that fraction, the risk factor, is where the geographic penalty happens.

If you are in San Francisco, your risk is pretty standard. But if you are in an emerging market, VCs add a hidden tax to your risk factor. In finance, this is called the "Country Risk Premium" (CRP).

Why do they add this tax? Because they are terrified of things you can't control:

- What if the local currency crashes against the US Dollar?

- What if the government suddenly changes corporate compliance laws?

- What if a giant US company wants to buy you, but their lawyers refuse to deal with the headache of a cross-border foreign acquisition?

Because the VC has to take on all these extra headaches, they increase your risk factor.

The Denominator Effect

Here is where the math bites you. Let's look back at our simple fraction:

Valuation = (Expected Future Exit) / (The Risk Factor)

Because the risk factor is at the bottom of the fraction (the denominator), making it bigger absolutely crushes your final valuation.

If a VC assigns a 15% risk rate to a US startup, the math works out fine. But if they assign a 35% risk rate to you because of that country risk premium, the math gets ugly fast. Over a 5-year timeline, dividing by that much larger risk number literally cuts your valuation in half.

It's not an insult. It's not bias. It is literally just how the formula works.

The Fix: "The Delaware Flip"

So, how do you fix it? You don't argue with the investor. You change the math.

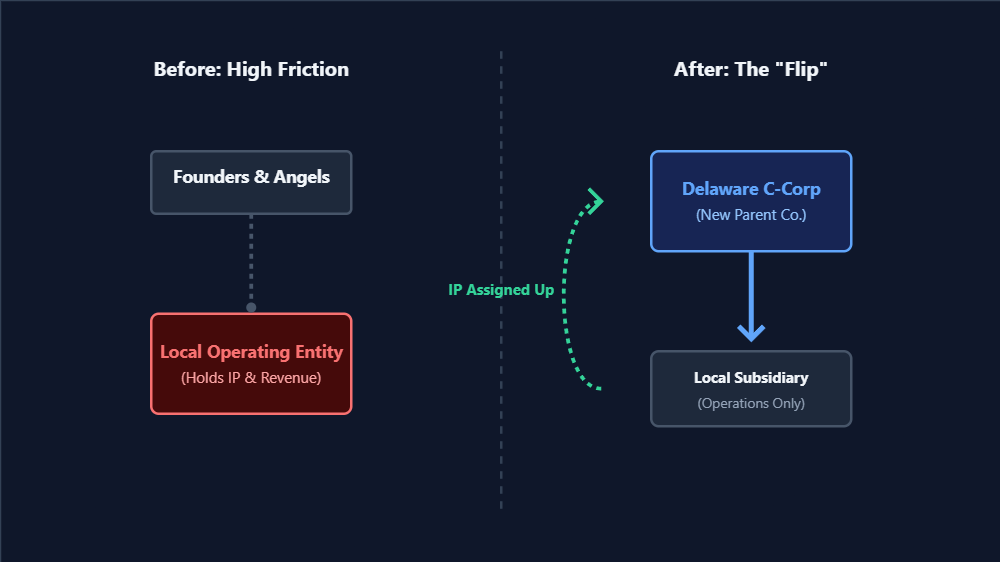

You do this by restructuring your company. In the startup world, this is called "The Delaware Flip."

You don't need to move your team to the US. Instead, you hire a lawyer to create a brand-new "Parent" company in Delaware (a US state with incredibly business-friendly laws).

You then legally make your local startup a subsidiary (a child company) of that new Delaware corporation. Finally, you take all your intellectual property, like your code and your brand, and officially assign it to the US company.

You have just put a US mask on your global company.

Now, when a VC looks at your pitch, they aren't investing in a foreign entity with unknown legal risks. They are buying standard US stock in a standard US company. If Google wants to buy you, they are buying a US company.

The country risk premium drops to zero. The bottom of the fraction shrinks back down to normal. Your valuation goes back up to $15 million.

The Ultimate Weapon: Geographic Arbitrage

Once you do the flip, something amazing happens. Your location stops being a penalty and transforms into the ultimate cheat code.

You unlock "Geographic Arbitrage."

Geographic arbitrage is simple: You make money in strong currencies like USD, but you pay your bills in a lower-cost local currency.

Imagine that San Francisco founder raises $2 million. They have to pay Bay Area rents and $150k starting salaries for junior developers. That $2 million might only last them 18 months before they go bankrupt.

You raise the exact same $2 million for your new Delaware C-Corp. But because your engineering team and operations are based in an emerging market, your monthly burn rate is drastically lower.

That exact same $2 million buys you 60 months of runway.

You just bought yourself three times the amount of time to build your product, make mistakes, and find your market. Capital is restricted by borders, but if you set up your company structure correctly, you can use those borders to make your startup mathematically unkillable.