When you are pitching a venture capitalist, it is incredibly easy to get caught up in the marketing. You see the polished website, the partner’s impressive Twitter threads, and the promise of a "value-add partnership." But behind the smiles and the term sheets lies a cold, mechanical reality: a ticking 10-year clock.

You aren’t just partnering with a person; you are entering into a highly specific financial vehicle with a hard-coded expiration date. If you don’t understand the math driving that vehicle, you will eventually get run over by it.

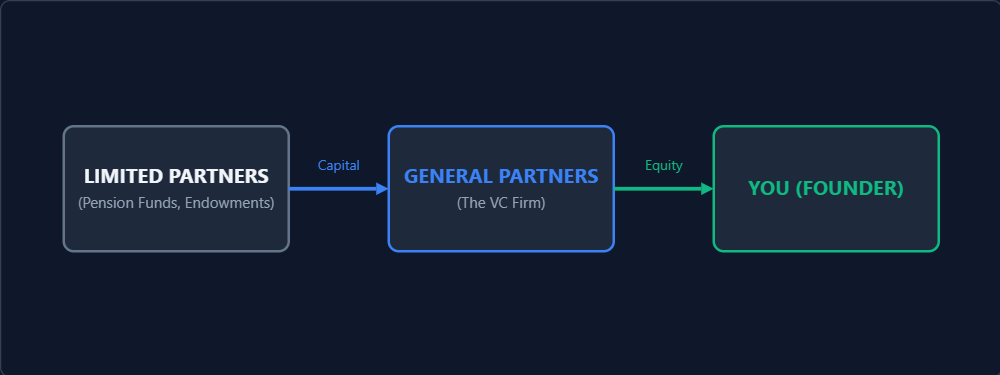

Before we look at the timeline, you have to understand the power dynamics. The money doesn’t belong to the VC.

Venture Capitalists (General Partners, or GPs) raise their capital from Limited Partners (LPs)—pension funds, endowments, and family offices. These LPs lock up their capital for a decade with the expectation of outsized returns. The GP’s entire job is to deploy that capital, multiply it, and return the cash before the clock runs out.

I. The Anatomy of the 10-Year Clock

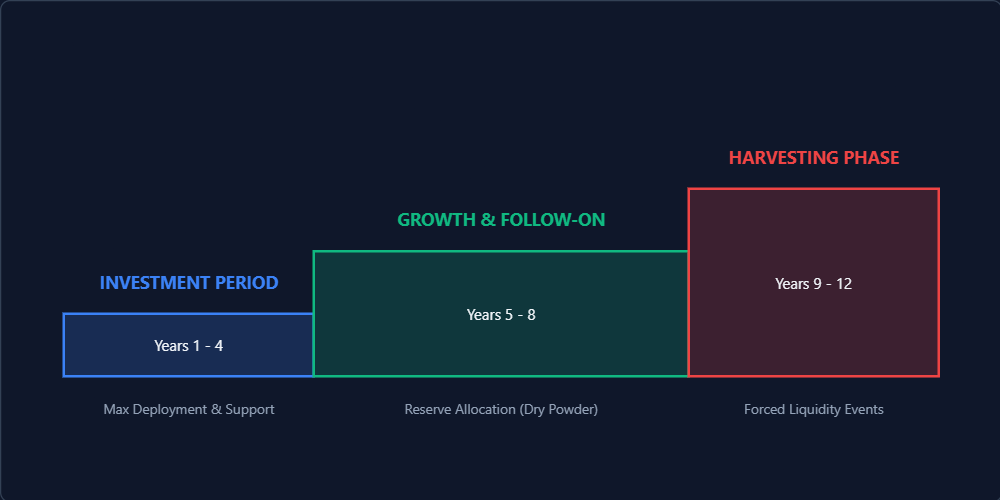

A standard venture fund is structured as a 10-year closed-end vehicle. This timeline is not a suggestion; it is a legally binding constraint that dictates every decision your board member makes.

Years 1–4: The Deployment Sprint In the beginning, the fund is in its "Investment Period." This is when alignment between founder and investor is at its absolute peak. The GP has a vault full of LP capital and a mandate to deploy it aggressively. They are writing checks, taking board seats, and searching for the outliers—the "fund returners." If you take money from a fund in Year 1, you have the maximum amount of runway before their structural pressure kicks in.

Years 5–8: Triage and The Squeeze By Year 5, the fund generally stops making net-new investments. The focus shifts entirely to portfolio management. The GP looks at their board and starts performing triage.

- The Follow-On: The clear winners receive massive follow-on funding from the firm's reserves to protect their pro-rata ownership.

- The Orphans: If your company is just doing "okay"—growing slowly or struggling to find product-market fit—you become an orphan. The VC won't write another check, and more dangerously, their lack of a follow-on check sends a negative signal to other investors.

Years 9–10+: The Harvesting Phase This is where the math gets brutal. The fund’s term is ending. LPs don't want paper markups; they want DPI (Distributed to Paid-In capital). They want actual cash returned to them.

- Forced Liquidity: If you are in Year 9 of a fund's lifecycle, your lead investor will start heavily pressuring you toward an exit—an M&A event, a secondary sale, or an IPO. Even if your company could be worth 5x more in another three years, the VC's clock is at zero. They need to sell today to close their books.

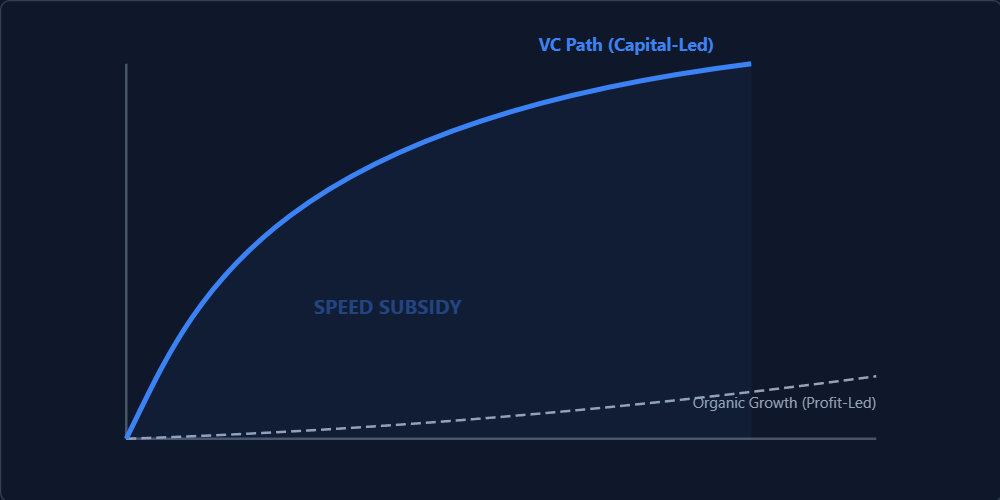

II. The Speed Subsidy: Buying a Head Start

If venture capital comes with this much structural baggage, why take it? Because venture capital is effectively a "speed subsidy." It is permission to operate unprofitably in exchange for capturing a market before your competitors can.

The Upside: Unnatural Growth Bootstrapped companies are constrained by their own revenue. If they make $100k, they can spend $100k. VC capital breaks this constraint. It allows you to hire a world-class engineering team, spin up massive cloud infrastructure, and acquire users at a scale your balance sheet has no business supporting. You are trading equity to buy a two-year head start on the future.

The Downside: Structural Fragility Sprinting breaks things. When a company is built entirely on subsidized speed, it often forgets how to build a sustainable business model. If the macroeconomic climate cools down and the VC subsidies stop flowing, companies that only know how to burn capital will violently collapse.

III. Playing the Game to Win

As a founder, you can use the VC engine to your advantage, provided you understand the mechanics.

1. Reverse Due Diligence (The Vintage Question) The most important question you can ask a VC during a pitch is: "What vintage is this fund, and where are you in your deployment cycle?" Taking a Series A check from a Year 1 fund means you have a long runway of patience. Taking that same check from a Year 6 fund means they are going to need you to exit much faster than you might be ready for.

2. Securing the Reserves When you negotiate a term sheet, you need to understand the firm's reserve strategy. For every dollar they invest in you today, how many dollars are they holding back to support you in the next round? A VC with no reserves cannot protect you during the "Squeeze" phase.

3. The Human De-Risking (Secondaries) At the Series B or Series C stage, smart founders push for secondary liquidity. Selling a small percentage (10-15%) of your personal shares turns you from a paper millionaire into an actual one. Once your personal financial survival is off the table, you become a bolder, more aggressive CEO who is willing to swing for the fences—which is exactly what the VCs want you to do anyway.

Venture capital is the most powerful accelerant in the business world, but it is purely a tool. Use it to build a category-defining product at 10x speed, but never forget that you are operating inside someone else's machine.